How it works

SILAC Teton Bonus Fixed Indexed Annuity: product description and policy

The Silac Teton Bonus Fixed Indexed Annuity offers the annuitant (annuity investor) an opportunity to earn a market index-linked return without incurring the risk of market downside. This might be a suitable plan for people who are approaching retirement and aim to grow and protect their retirement savings. This plan is also suitable for retirees who are looking for good accumulation potential and an optional Rider for enhanced liquidity benefits.

Let’s have a look at the high-level fine print of Silac Teton Bonus Fixed Indexed Annuity, and then we will discuss each point in detail.

| Product Name | Teton Bonus Fixed Indexed Annuity |

|---|---|

| Issuing Company | [Silac Insurance Company](https://annuityrateshq.com/reviews/silac-annuity-reviews) |

| AM Best Rating | B (7th of 13 ratings) |

| Withdrawal Charge Period(s) | 5, 7, 10 and 14 years |

| Maximum Issue Age | 90 Years for 5 -and 7-year withdrawal charge period. 85 Years for 10-year withdrawal charge period. 80 Years for 14-year withdrawal charge period. |

| Minimum Initial Purchase Amount | $10,000 |

| Surrender Charge Schedule | Varies for different tenure policies |

| Initial Premium Bonus | Yes |

| Crediting Period and Strategies | - **1-year** point-to-point with participation rate or caps - Monthly point-to-point with cap - Monthly average with participation rate - 1-year point-to-point with boost - 1-year fixed with interest rate guaranteed |

| Plan Types | - IRA - Roth IRA - Nonqualified Account - SEP IRA - SIMPLE IRA - 401(a) |

| Indexes | - S&P 500 Index - S&P 500 Duo Swift Index - S&P 500 RavenPack Index - Barclays Atlas 5 Index - Nasdaq Gen 5 Index - Bloomberg Versa Index |

| Free Benefits | - Terminal Illness - Nursing Home Benefit - Home Health Care benefit |

| Additional Benefits | Free withdrawals can be carried forward to the next policy year |

| Free Withdrawals | 5% of the annuity’s Accumulated Value; per year. |

| Death Benefit | Beneficiary(s) will receive the full Account Value upon the death of the Owner with no surrender charges |

| Riders | Optional Enhanced Liquidity and Bonus Riders (Elevation and Elevation Plus) |

| Surrender Value | Greater of Accumulated Value (less any withdrawal charges/MVA) and the Minimum Guaranteed Surrender Value |

| RMD Friendly | Yes |

The Silac Teton Bonus Fixed Indexed Annuity is almost identical for all policy tenures, except the crediting strategies and surrender charge schedule. For ease of discussion and better clarity, we will discuss the Silac Teton Bonus 10 Fixed Indexed Annuity (unless mentioned otherwise) for the rest of the article.

How does the Silac Teton Bonus Fixed Indexed Annuity policy work?

Any annuitant (maximum age at the time of policy issue: 85) can purchase the Silac Teton Bonus 10 fixed indexed annuity with a minimum initial purchase amount of $10,000, and in return, they will earn market index returns (calculated through a formula that we will discuss shortly), credited as per the chosen crediting period. Apart from the regular crediting period, there are various events that may trigger earnings credit: On free withdrawals, for a long-term care event or terminal illness or injury event, or when a death benefit is payable. All these interest credits are credited to a bucket called “Account Value.” This bucket is your annuity account balance, and all your withdrawals take place from it. In this bonus version of the annuity, a premium bonus is added to the initial premium depending on the withdrawal charge period.

At the time of this review (Sep 2024), this was the published figure. For current rates, see Current Rates ↑.

- 5-year withdrawal charge period: 7% bonus

- 7-year withdrawal charge period: 10% bonus

- 10-year withdrawal charge period: 15% bonus

- 14-year withdrawal charge period: 15% bonus (for most states)

This bonus is designed to boost the initial Account Value, providing a more substantial foundation for your retirement income, especially beneficial for those who begin their annuity during these age ranges.

Growth of Account Value

The Silac Teton Bonus 10 Fixed Indexed Annuity offers the annuitant to choose from one or more of the six indexes (S&P 500 Index, S&P 500 Duo Swift Index, S&P 500 RavenPack Index, Barclays Atlas 5 Index, Nasdaq Gen 5 Index, Bloomberg Versa Index) to determine their earnings crediting formula. Each index has multiple strategies to choose from. The plan also offers a fixed-rate guaranteed interest strategy to choose from, making a total of 12 strategy options. We will discuss each available index briefly:

1. S&P 500 IndexThe S&P 500 index is one of the most popular and oldest indexes in the world. It tracks 500 large-cap publicly traded stocks listed in the United States. It is a reliable index and has often succeeded in the test of time. It is very important to note that, similar to most other annuities, the Silac Teton Bonus Fixed Indexed Annuity offers the S&P 500 index with caps, participation rates, and spreads in place, meaning that your interest-earning capacity is limited. These rates change frequently; I will discuss the rates in detail shortly.

2. S&P 500 Duo Swift IndexThe S&P 500 Duo Swift Index is a specialized financial index designed to measure the performance of a controlled volatility version of the S&P 500. This index incorporates a risk control mechanism that operates on S&P 500 E-mini futures and includes a 10-year U.S. Treasury Bond futures overlay. The primary objective of the index is to manage volatility and reduce path dependency, making it a dynamic tool for investors seeking stability in volatile markets. While these volatility controls may lead to less fluctuation in returns compared to indices without such mechanisms, they also lower the potential overall rate of return in comparison to those other indices.

3. Barclays Atlas 5 IndexThe Barclays Atlas 5 Index is a global financial index designed to provide stable and consistent returns through a diversified portfolio of equities and bonds from around the world. The Atlas 5 Index offers investors an opportunity to participate in approximately 90% of the global economy, expanding beyond the U.S.-centric focus of indices like the S&P 500. It aims to achieve this by targeting a 5% volatility level, utilizing techniques from Modern Portfolio Theory and Momentum Investing to optimize its component allocations daily. The index's dynamic structure allows it to adjust its exposure between equities and bonds depending on market conditions, potentially being fully uninvested if the risk/reward scenario is deemed unfavorable. Similar to any volatility-controlled index, this may lead to less fluctuation in returns compared to indices without such mechanisms; they also lower the potential overall rate of return in comparison to those other indices.

4. S&P 500 RavenPack AI IndexThe S&P 500 RavenPack AI Index is a financial index that leverages artificial intelligence to analyze news sentiment and apply it to a sector rotation strategy within the S&P 500. Developed by S&P Dow Jones Indices in collaboration with RavenPack, the index measures exposure to the S&P 500 RavenPack AI Sentiment Index, which identifies sectors with the highest sentiment scores based on news analytics. The index employs a multi-asset approach, combining U.S. equities and fixed income, and incorporates a daily risk control mechanism to maintain a target volatility of 5%. Similar to any volatility-controlled index, this may lead to less volatility in returns compared to indices without such mechanisms; they also lower the potential overall rate of return in comparison to those other indices.

5. Nasdaq Gen 5 IndexThe Nasdaq Generations 5 Index is a multi-asset, risk-controlled index designed to provide exposure to both the Nasdaq-100 Total Return Index and the Nasdaq Next Generation 100 Total Return Index. It also includes allocations to 10-year and 2-year U.S. Treasury futures, aiming to maintain a constant 5% volatility target. This index utilizes the truVol® Risk Control Engine, developed by Salt Financial, to dynamically manage allocations between its components and cash, enhancing its responsiveness and accuracy in volatility targeting. While this volatility-controlled mechanism causes less fluctuation in returns compared to indices without such mechanisms, it also lowers the potential overall rate of return in comparison to those other indices. The index is structured as a 70/30 blend of the Nasdaq-100 and the Nasdaq Next Generation 100 Indexes, with the remainder allocated to fixed income or cash.6. Bloomberg Versa IndexThe Bloomberg Versa 10 Index is a recently launched multi-asset benchmark specifically designed to address the evolving needs of the fixed indexed annuity market. It aims for a 10% volatility target by dynamically allocating its exposure across four major asset classes: US equities, US Treasuries, gold, and the US dollar. Each of these asset classes is tracked through its own dedicated volatility-targeted sub-index, allowing the index to respond in real time to changing market conditions and to balance performance with stability.

Note: In addition to allocating the funds in the following indexes, the annuitant also has the option to allocate funds at a fixed interest. The Fixed Value Rate for the 10-year withdrawal charge period at the time of writing this article was 3.00%. These Fixed Rates change from time to time. You can contact your trusted financial advisor to know the latest rates.

Rates and costs

Rates, bonus, surrender charges, and costs

As mentioned earlier, all earnings, whether in the form of index credits or fixed rate credits, are credited to the "Account Value" bucket. However, it’s important to note that we do not receive the full index return in our account. This section explains how these index returns are calculated and added to our account value.

The Earnings Crediting Formula

The earnings crediting formula is a crucial aspect of this annuity discussion. It’s essential to understand that the index return is not directly credited to our annuity. Instead, factors such as participation rates, cap rates, and spreads/boosts set by the company influence our earnings. These rates can change over time, so it’s advisable to consult with your trusted financial advisor for the latest rates.

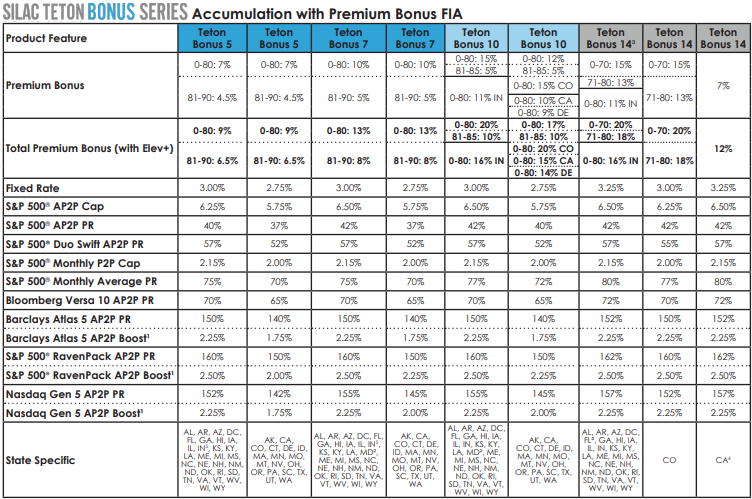

Let’s have a look at the Silac Teton Bonus Fixed Index Annuity rate sheet (as of July 2025) to understand how the earnings are determined.

From the above rate chart, you will notice that there are 13 interest crediting options (1 fixed and 12 indexed). Let’s have a look at different terms that are used by the company in the Teton Bonus Fixed Indexed Annuity chart rate:

Participation Rate

The participation rate describes the annuitant’s participation percentage in a return of an index. For example, suppose the participation rate is 150%, and the index returned 4% over the agreed time. In that case, the annuitant will be eligible for 150% of the return, i.e., 6%.

Participation Rate simulator

Shows how the contract credits a percentage of a positive index return.

5%

Formula

10% x 50% = 5%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

Cap Rate

This refers to the rate at which your interest-earning capacity is capped. For example, if an index returns 12% but the contract’s cap rate is 6%, the annuitant will be eligible for an interest credit of 6% only. It doesn’t matter how much the index goes above the cap rate; the maximum interest that can be earned is the cap rate.

Cap Rate simulator

Shows how a cap limits the credited return when the index year is higher than the selected cap.

8%

Formula

min(10%, 8%) = 8%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

One-Year Monthly Index Average with Participation Rate

This strategy begins by recording the initial value of a selected index at the onset of the contract term. Subsequently, the index's value is captured monthly. After a one-year duration, these monthly index values are aggregated and then averaged by dividing the total by 12. This average, multiplied by the participation rate, helps decide the interest added to the annuity.

Point-to-point with Boost

The amount of interest that the Company will credit is based on a declared boost on the selected index on an annual point-to-point basis. Once the index gain is determined (if any), the boost amount is added. The remaining amount is what is credited to the contract for that term.

Fixed Account Rate

If you opt for a fixed account rate, you simply earn the fixed rates for a particular period specified by the company before your policy begins. These rates are usually low/at par as compared to other fixed avenues, such as CDs and MYGAs, so you should avoid fixed rates in a general scenario. The 1-year fixed rate on this policy at the time of writing this article was 3.00%.

When allocating premiums in a fixed-indexed annuity, individuals can distribute their money across these different indexing strategies. This means you can decide how much of your premium goes into each strategy, allowing for a tailored approach to potential growth and risk based on your financial goals and comfort level.

Among these indices, I prefer the following strategies (as of July 2025):

- S&P 500 Annual Point-to-Point with Cap: Due to the proven historical track record of the S&P 500 index and a relatively higher cap rate. It's important to note that the S&P 500 Index is different from the S&P 500 Duo Swift and the S&P 500 RavenPack indices, which are volatility control indices.

- Barclays Atlas 5 Annual Point-to-Point with Participation Rate: This strategy is favored because of the high participation rate it offers.

- Nasdaq Gen 5 Annual Point-to-Point with Boost: I prefer this strategy due to its high Boost rate and the high quality of the index.

It’s important to note that there is also a standard version of this annuity, the Teton Fixed Indexed Annuity, which does not include any bonus. However, the bonus version has some trade-offs: while you receive an 11% initial bonus on the “Account Value” account, a closer look at the rate charts reveals that the bonus version offers slightly lower participation rates, cap rates, and other related factors.

Furthermore, in the Teton Bonus Fixed Indexed annuity with Elevation Plus rider, the Account Value grows at an additional 5%, making the total premium bonus 20% (15 + 5%) of the initial premium paid. Thus, each option has its pros and cons, and your decision should depend on whether you prioritize the upfront bonus or prefer the potential for higher long-term growth with more favorable participation rates and a higher growth multiplier.

Carrier

Company details

You must always keep in mind that, unlike CDs, annuities are not guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other federal insurance agency. An annuity's "guarantee" is only as strong as the insurance company that issues the annuity, so it is always important to assess the issuing company before buying an annuity.

Silac Insurance Company

SILAC Insurance Company, originally founded as Equitable Life & Casualty Insurance Company in 1935, is Utah's oldest active life insurance company. The company, headquartered in Salt Lake City, Utah, has a rich history of providing life and health insurance, particularly focusing on the needs of seniors. In 2018, SILAC entered the annuity market, expanding its offerings to include a variety of innovative annuity products, such as Fixed Index Annuities and Multi-Year Guaranteed Annuities. SILAC is licensed to operate in 48 states and the District of Columbia, making it a significant player in the national insurance market.

It is rated as follows by the rating agencies:

| Rating Agency | Rating |

|---|---|

| AM Best | B (7th of 13 ratings) |

| KBRA | BBB |

SILAC's credit ratings reflect a moderate level of financial stability and suggest adequate creditworthiness. While SILAC is financially sound, it's important to consider its overall financial strength compared to higher-rated insurers. As of year-end 2024, some of the financial highlights for SILAC Insurance Company include its:

- $4.4 billion in total cash and invested assets

- $738 million of total adjusted capital and surplus

- $14.8 billion in-force account value

- 120,000 plus policyholders

Pros

Good Annuity for Accumulation

The Teton Bonus Fixed Indexed Annuity offers strong potential for accumulation, featuring a generous starting bonus along with competitive cap rates, participation rates, and boost rates.

Cumulative Free Withdrawals

If no withdrawals are taken in a given year, fully unused free withdrawals can be carried over to the next policy year up to the maximum cumulative free withdrawal percentage.

Free Terminal Illness, Nursing Home, and Home Health Care Benefits

The inclusion of these benefits at no additional cost provides crucial financial support in the event of serious health challenges. With the ability to access up to 100% of your account value under certain conditions, this product offers peace of mind during difficult times.

No Annual Contract, Mortality & Expense, or Administrative Fees

Multiple Payout Options

The Teton Bonus Fixed Indexed Annuity provides flexibility in how you receive your payouts, whether through a lump sum or various annuitization options, such as Life Only, Life with Period Certain, or Joint and Survivor Life.

Cons

Lower Free Withdrawal Limit

During the withdrawal-charge period, the annuity allows for standard free withdrawals of only 5% of the account value, which is lower than many competitors that typically allow for 10% free withdrawals. However, you can access 10% free withdrawals if you opt for any of the optional riders, though it comes with an additional cost.

Cost Consideration of the Riders

While the Riders offer enhanced liquidity benefits, the cost could have been somewhat lower, making it a more attractive option for those looking to access higher liquidity from their annuity without incurring significant additional expenses.

Conclusion

Conclusion

With advancements in healthcare and technology, the average American today lives longer than ever. Consequently, it's crucial to have a source of income that grows safely and steadily, and can provide a guaranteed income during retirement years. This strategy not only mitigates the risk of outliving your income but also ensures a decent standard of living in retirement.

The Teton Bonus Fixed Indexed Annuity offers a well-rounded package of features designed to provide flexibility, security, and financial support throughout retirement. With its relatively higher accumulation potential, terminal illness, nursing home care, and home health care benefits, this product ensures that annuitants have access to their funds when they need them most. The optional paid “Elevation” riders further enhance its appeal, making it a strong choice for those who want higher liquidity from their annuity.

However, potential buyers should weigh these benefits against certain drawbacks, such as the lower free withdrawal limit during the withdrawal-charge period. Additionally, while SILAC's credit ratings indicate adequate financial stability, prospective annuitants should consider the company's ratings in comparison to other insurers. Importantly, this annuity may not be the best suited for those primarily focused on leaving a legacy, as its structure is more geared toward accumulation and liquidity. As with any financial product, it’s advisable to thoroughly review the details and consult with a financial advisor to ensure that it aligns with your specific retirement goals and needs.