Introduction

Like every other day, before you pull into your driveway you check the mailbox for the day’s bills, marketing mailers, etc. You notice that there’s an envelope from an insurance company you recently bought an annuity from. Inside is the very first statement for the annuity you purchased through them.

In general, it’s understood that annuities are complex products. Now that you’ve bought one, you’ll have to navigate this document full of annuity industry jargon, legal-ese and acronyms.

This article aims to give you a better understanding of how to read your annuity statement and what to look for.

What is an annuity statement?

An annuity statement offers a snapshot of your investment’s performance over time, highlighting critical values like current cash value, surrender value, and guaranteed withdrawal amounts. However, these statements can be complex, with confusing terms, making it important to carefully review and understand each section.

Fees and charges — such as mortality expenses, investment fees, and potential state taxes — can significantly affect returns, particularly in variable annuities. Understanding your death benefit value is critical for estate planning, ensuring beneficiaries receive financial protection. The lifetime income value informs how much you can sustainably withdraw during retirement.

Other important factors include market value adjustments (MVAs) for early withdrawals and participation rates for fixed index annuities, which determine how much of market gains are credited to your account.

Regularly reviewing your annuity’s actual earnings vs. promised earnings helps ensure the investment meets expectations. If the information feels overwhelming, consulting a trusted financial advisor can help you better understand your statement and make informed decisions.

Ultimately, consistently reviewing and understanding your annuity statement empowers you to manage your financial future confidently.

Start with the Basic Information

It may seem obvious, but annuity statements can contain simple errors. So always start off with confirming the account holder information: name contract number, issuing company, etc.

It’s also important to review key dates and ensure their accuracy: purchase date, anniversary date, surrender charge schedule timeline, etc.

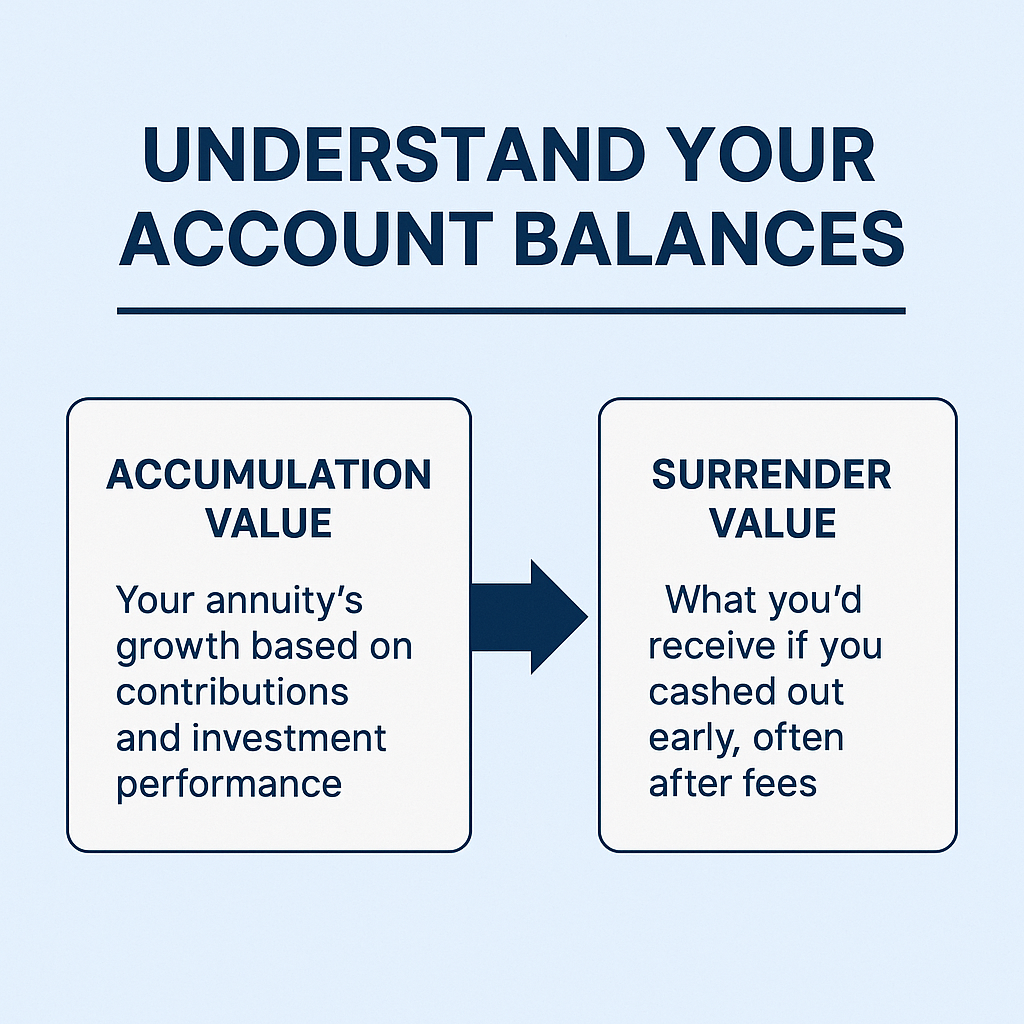

Understand Your Account Balances

Key areas to focus on here include the accumulated value (your annuity's growth) versus the surrender value (what you’d receive if you cashed out early, often after fees). Fixed and variable annuities behave differently, with variable annuities experiencing more market-driven fluctuations. A guaranteed rate of return provides a safety net, especially important for retirees seeking steady income.

Accumulation Value

The accumulation phase of an annuity is the period of time the funds build before paying out. This number should represent the current value based on contributions and any investment performance. It’s important to understand the type of annuity you must ensure this value is correct based on your contributions and how the market has performed. Pay close attention to the minimum rates of return guaranteed in the contract and any rate caps that may apply.

Surrender Value

The surrender value is the value of the annuity or payment if you were to withdraw from your annuity prior to the contract accumulation phase. There is typically a schedule associated with an annuity with larger fees at the beginning of the accumulation phase and gradually getting smaller until the accumulation phase ends.

It’s typically not recommended to withdraw funds early from an annuity since the surrender fees can be quite large (upwards of 10%). But hardship withdrawals can sometimes be made depending on the contract. If you are faced with a potential early withdrawal, it is important to understand this section of the annuity statement well.

Identify the Guaranteed Values

Depending on the contract and riders associated with the annuity, “guaranteed value” could mean several different things. Below is a list of possible meanings and their descriptions. Understanding this value is crucial for planning, as it identifies the income sources that provide a reliable foundation for developing a retirement income strategy.

| Guaranteed Minimum Value | Description |

|---|---|

| Guaranteed Minimum Withdrawal Benefit (GMWB) | Ensures the account holder can withdraw a minimum amount from the annuity, usually a percentage of the initial investment, regardless of market performance. |

| Guaranteed Minimum Income Benefit (GMIB) | Provides a minimum level of income payments for the annuitant, regardless of the annuity's investment performance, after a certain waiting period. |

| Guaranteed Minimum Accumulation Benefit (GMAB) | Ensures that the account holder will receive at least the initial investment amount after a specified period, even if the market performs poorly. |

| Guaranteed Minimum Death Benefit (GMDB) | Offers a minimum death benefit to the annuitant's beneficiaries, which can be the initial investment or the accumulated value, whichever is higher. |

Review Investment Performance (for Variable or Indexed Annuities)

Fixed annuities guarantee the same rate or return for the life of the annuity no matter the fluctuations in the broader markets. But variable annuities and indexed annuities will mirror the broader market. These annuities will have a section in their statements detailing the performance of their underlying investments.

| Aspect | Variable Annuities | Indexed Annuities |

|---|---|---|

| Underlying Investments | Subaccounts invested in mutual funds or other securities | Track a specific index, such as the S&P 500, with returns linked to index performance |

| Investment Performance | Can vary significantly depending on market performance | Returns are based on index performance but may have caps or participation rates |

| Risk | Higher risk due to direct market exposure | Moderate risk with some downside protection, but potential returns may be limited |

| Volatility | High volatility, reflecting the underlying securities | Lower volatility compared to variable annuities, but still influenced by market movements |

| Fees | Mortality and Expense (M&E) risk charges, administrative fees, investment management fees for underlying funds | Typically, lower than variable annuities, may include administrative fees and rider fees |

| Potential Payouts | Potentially higher, but with greater risk | Potentially lower, but with more predictability and less risk |

Key considerations for when reviewing this section include:

- Analyze individual subaccount performance.

- Compare index returns to your credited returns (for indexed annuities).

- Check for volatility and risk indicators tied to market performance.

- Understand how performance impacts both accumulated value and potential payouts.

Examine the Fees and Charges

Types of Fees Listed

Be sure to know what fees and charges could be associated with your annuity. Below is a table of possible fees and charges to understand. If these fees/charges are applicable but not clear on the statement, be sure to contact the agent or insurance company for further clarification. Over time, fees will erode the growth of the underlying investments.

| Fee/Charge | Description |

|---|---|

| Mortality and Expense (M&E) risk charges | Charges covering the insurance risks and costs associated with annuity contracts. |

| Administrative fees | Fees for the administrative services provided by the annuity issuer. |

| Investment management fees for underlying funds | Fees for managing the investments within the annuity's underlying funds. |

| Rider fees for optional benefits | Additional charges for optional benefits added to the annuity contract. |

| Surrender charges | Fees for withdrawing funds early from the annuity, often decreasing over time. |

Check the Death Benefit Value

Many insurance companies offer death benefit riders in the case of the death of the annuitant. This may be provided as either a lump sum payment or a series of payments to designated beneficiaries. This consideration becomes particularly significant during estate planning to ensure that beneficiaries are properly named and in place.

Look for Market Value Adjustment (MVA) Details

An MVA applies when you withdraw funds from your annuity before a specified term ends, adjusting the value based on interest rate changes since the contract's initiation, which can either increase or decrease the surrender value. If interest rates have risen, the MVA may reduce the amount received upon early surrender, but if rates have fallen, it might increase the value. This adjustment protects the annuity issuer from market fluctuations. Understanding the terms under which the MVA is triggered, and how interest rates affect your annuity's value, is crucial. Additionally, most annuities offer penalty-free withdrawals after a set period or under specific conditions, avoiding unnecessary MVA penalties and providing some liquidity. By examining these aspects, you can navigate the complexities of the MVA section in your annuity statement and make informed decisions aligned with your financial goals.

Understand Participation Rates, Caps, and Spreads (for Fixed Index Annuities)

A participation rate is a percentage that defines the amount of the index's increase credited to your annuity. For example, if the index were to increase by 10%, but your participation rate (also called par rate) is 80%, then your annuity will only increase by 8%.

Caps help protect to the insurance company from too much upside by capping the maximum return you can get for your annuity. Typically, the tradeoff for the annuitant is that by capping the potential growth, your investment is better protected from market downturns.

Spreads are like participation rates since both limit the potential growth of the annuity. Spreads typically represent a percentage point difference that’s deducted from the gain of an index. For example, if an index were to grow by 10% and the spread is 2%, the annuity will only grow by 8%.

Prior to purchasing an annuity, it is important to balance par rates, caps, and spreads. Additionally, one must review the statement for the underlying investments and verify the initially contracted rates and spreads.

Compare Actual Earnings vs. Initial Projections

Most likely, during the initial phases of the annuity purchase, there was an initial projection of the annuity and the payouts. Getting an annuity statement would be the time to review the earnings and compare against the originally promised returns. Look for any discrepancies and potential causes (market changes, fees, etc.). And track the earnings over time and adjust your strategies accordingly.

Contact a Professional if Needed

When it makes sense to consult with a financial advisor, it's essential to work with fiduciaries who can provide unbiased advice. Engaging a professional can help you navigate your annuity statement and ensure you understand all the elements involved. Make sure to ask your advisor pertinent questions based on the findings in the statement, such as clarifying discrepancies, understanding market impact, and verifying projected versus actual returns. This collaborative approach can lead to better financial decisions and more control over your investments.

Conclusion

Understanding your annuity statement is crucial for managing your investments effectively. Start by reviewing the participation rates, caps, and spreads associated with your fixed index annuities to ensure you are balancing the potential growth and protection of your investment. Compare the actual earnings against the initial projections to identify any discrepancies and understand the reasons behind them, such as market changes or fees. Consulting with a financial advisor can provide valuable insights, especially if there are any discrepancies or if you need clarification on market impacts and projected returns. Regularly reviewing your annuity statements and addressing any questions early on will lead to better financial decisions and more control over your investments. A better understanding will lead to stronger financial control and fewer surprises.

Related on AnnuityRatesHQ