How it works

TruStage ZoneChoice Registered Index Linked Annuity: product description and policy

The TruStage ZoneChoice RILA Annuity is designed to provide policyholders with flexibility, growth potential, and a level of downside protection. It is best suited for individuals seeking higher growth potential than a fixed indexed annuity, with customizable downside protection to limit losses. It appeals to pre-retirees and retirees who want market exposure while maintaining control over their risk level. Let’s have a look at the high-level fine print of the TruStage ZoneChoice Annuity, and then we will discuss each point in detail.

| Product Name | ZoneChoice Annuity |

|---|---|

| Issuing Company | MEMBERS Life Insurance Company |

| AM Best Rating | A (3rd of 13 ratings) |

| Withdrawal Charge Period(s) | 6 years |

| Maximum Issue Age | 85 Years |

| Minimum Initial Purchase Amount | $5,000 |

| Crediting Period and Strategies | - 1-year point-to-point with participation rate - 1-year point-to-point with caps - 2-year point-to-point with participation rate - 1-year fixed with interest rate guaranteed |

| Plan Types | - IRA - Roth IRA - Nonqualified Account - SEP IRA - SIMPLE IRA - 401(a) |

| Indexes | - S&P 500 Index - Dimensional US Small Cap Value Systematic - Barclays Risk Balanced Index |

| Free Withdrawals | 10% of the annuity’s Accumulated Value per year |

| Death Benefit | Return of Purchase Payment or Contract Value, whichever is higher, without any surrender charges |

| Free Benefits | - Nursing Home and Terminal Illness Waivers |

| Riders | No optional riders |

| Surrender Value | Account Value less any withdrawal charges/ MVA |

| Minimum Guaranteed Surrender Value | Return of Purchase Payments |

How Does the TruStage ZoneChoice Annuity Work?

The TruStage ZoneChoice Annuity is a Registered Index-Linked Annuity (RILA) that provides a combination of market-linked growth, downside protection, and customizable features. It allows policyholders to balance risk and reward by selecting from multiple allocation options, including indexed and fixed-rate accounts. Here’s a detailed breakdown of how it works:

Initial Setup and Funding

- Minimum Payment: $5,000

- Maximum Payment (Without Prior Approval): $999,999

- Issue Age: 21 to 85 years old

- Plan Types: Traditional IRA, Roth IRA, SEP IRA, Beneficiary IRA, Non-Qualified, Non-Qualified Beneficiary (Stretch)

After making an initial payment, policyholders have the flexibility to choose how their funds will be allocated across various indexed accounts or the declared rate account. These allocation choices play a major role in how the annuity performs over time. Apart from the regular crediting period, there are various events that may trigger earnings credit: On free withdrawals, for a long-term care event or terminal illness or injury event, or when a death benefit is payable. All these interest credits are credited to a bucket called “Account Value.” This bucket is your annuity account balance, and all your withdrawals take place from it.

The TruStage ZoneChoice Annuity offers the annuitant to choose from one or more of the three indexes (S&P 500 Index, Dimensional US Small Cap Value Systematic, and Barclays Risk Balanced Index) to determine their earnings crediting formula:

- The Standard & Poor's 500 (S&P 500) is a stock market index that tracks the performance of 500 large-cap U.S. companies across various industries. It serves as a key indicator of the overall health of the U.S. equity market and is widely used as a benchmark for investment performance.

- The Dimensional US Small Cap Value Systematic Index focuses on small-cap U.S. companies that exhibit value characteristics, such as lower price-to-book ratios. It aims to capture the value premium by systematically targeting smaller, undervalued firms, offering exposure to a segment of the market with potential for higher returns.

- The Barclays Risk Balanced Index is part of a diverse family of systematic, non-discretionary trading strategy indices available across multiple asset classes, including equities, fixed income, FX, commodities, derivatives, and alternative investments.

Account Options

The allocation can be spread across 11 risk-controlled accounts and one Declared Rate Account. These include a mix of 1-year and 6-year term accounts.

1-Year Accounts (Annual Reset, Lock-in Gains)

- 1-Year Declared Rate Account

- S&P 500 Index (Adjustable Floor + Cap)

- S&P 500 Index (-10% Buffer + Cap)

- Dimensional US Small Cap Value Systematic Index (Adjustable Floor + Cap)

- Dimensional US Small Cap Value Systematic Index (-10% Buffer + Cap)

- Barclays Risk Balanced Index (Adjustable Floor + Cap)

6-Year Accounts (Higher Growth Potential, Participation Rate)

- S&P 500 Index (-10% Buffer, Participation Rate)

- Dimensional US Small Cap Value Systematic Index (-10% Buffer, Participation Rate)

- Barclays Risk Balanced Index (-10% Buffer, Participation Rate)

- S&P 500 Index (-20% Buffer, Participation Rate)

- Dimensional US Small Cap Value Systematic Index (-20% Buffer, Participation Rate)

- Barclays Risk Balanced Index (-20% Buffer, Participation Rate)

The 6-year accounts offer the potential for higher returns through participation rates, while the 1-year accounts provide more flexibility by allowing annual adjustments and lock-in gains.

Rates and costs

Rates, bonus, surrender charges, and costs

The Earnings Crediting Formula

The earnings crediting formula is the most important part of this annuity discussion. It is important to know that we don’t simply get the index return credited to our annuity. There are a few rates, caps, and other rates that the company has in place that affect your earnings. These rates tend to change over time, and the updated rates can always be checked on the company’s website.

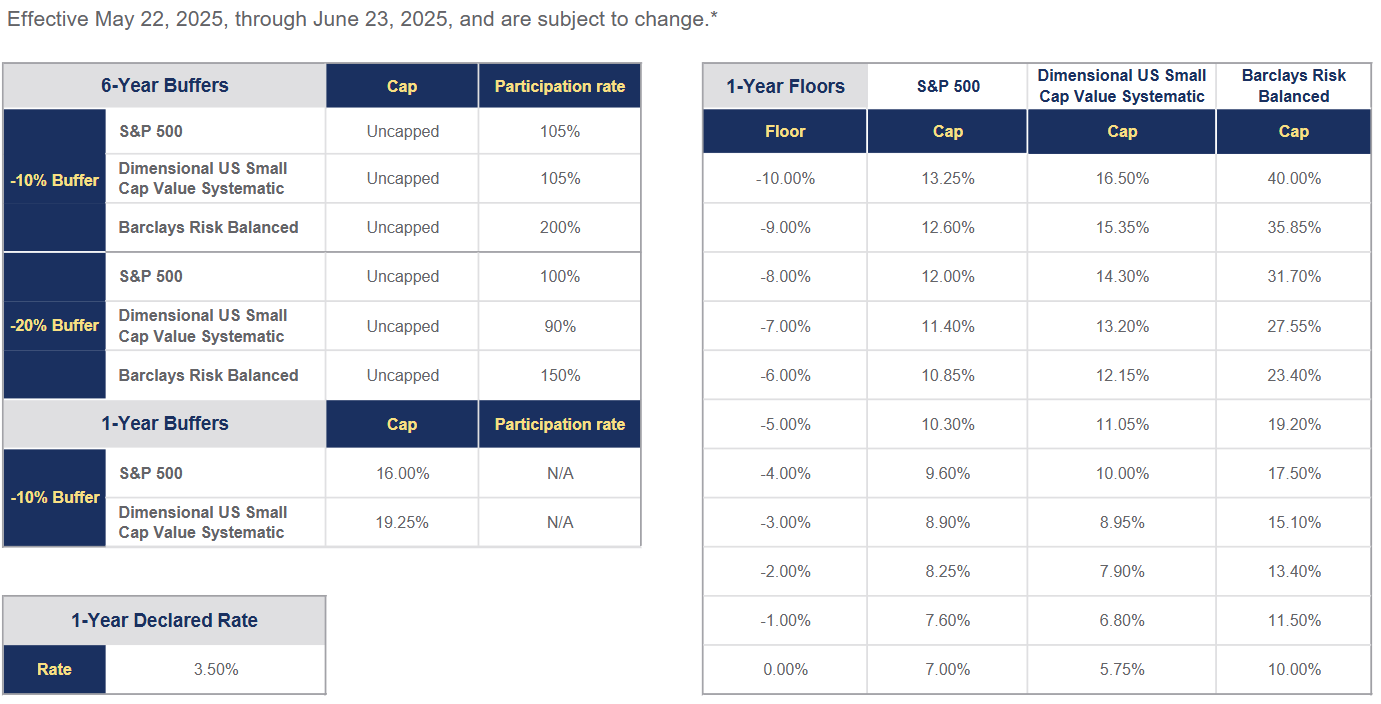

Let’s have a look at the TruStage ZoneChoice Annuity rate sheet (as of May 2025) to understand how the earnings are determined.

From the above rate chart, you will notice that there are 12 interest crediting options (1 fixed and 11 indexed). Let’s have a look at different terms that are used by the company in the TruStage ZoneChoice chart rate:

Participation Rate

The participation rate describes the annuitant’s participation percentage in a return of an index. For example, suppose the participation rate is 150%, and the index returned 4% over the agreed time. In that case, the annuitant will be eligible for 150% of the return, i.e., 6%.

Participation Rate simulator

Shows how the contract credits a percentage of a positive index return.

5%

Formula

10% x 50% = 5%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

Cap Rate

This refers to the rate at which your interest-earning capacity is capped. For example, if an index returns 12% but the contract’s cap rate is 8%, the annuitant will be eligible for an interest credit of 8% only. It doesn’t matter how much the index goes above the cap rate; the maximum interest that can be earned is the cap rate.

Cap Rate simulator

Shows how a cap limits the credited return when the index year is higher than the selected cap.

8%

Formula

min(10%, 8%) = 8%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

Fixed Account Rate

If you opt for a fixed account rate, you simply earn the fixed rates for a particular period specified by the company before your policy begins. These rates are usually low/at par as compared to other fixed avenues, such as CDs and MYGAs, so you should avoid fixed rates in a general scenario. The 1-year fixed rate on this policy at the time of writing/updating this article was 3.50%.

Risk Control Customization

Policyholders can choose from two key risk control mechanisms: Buffers and Floors.

- Buffers: A buffer protects you from a certain percentage of market losses before you experience a loss in your account value.Example: With a -10% buffer, if the market drops 15%, the policyholder only absorbs a 5% loss. If the market drops 8%, the entire loss is absorbed by the buffer, and no loss is incurred.

- Floors: A floor sets the maximum amount of loss the policyholder is willing to absorb. Losses below this limit are absorbed by the insurer.Example: With a -10% floor, if the market drops 30%, the policyholder only loses 10%, and the remaining 20% loss is absorbed by the insurer.

These tools allow policyholders to tailor their investment strategy based on their risk tolerance and market outlook.

Interest Crediting Strategy

The interest credited to the annuity depends on the performance of the indices chosen and the specific account allocation.

- 1-Year Accounts: Interest is credited annually, and gains are locked in, meaning that once interest is credited, it cannot be lost due to future market declines.

- 6-Year Accounts: These accounts use a participation rate rather than a cap. The growth is linked to the performance of indices like the S&P 500, and the participation rate determines how much of the index's growth is applied to the account.

For example, if the participation rate for the S&P 500 is 120%, and the index grows by 10%, the policyholder's account value grows by:

10% x 120% = 12%

If the market performs poorly, the buffer or floor will limit the downside loss, as discussed earlier.

At the end of every interest term, policyholders can reallocate their funds to different accounts. The process is straightforward and allows for ongoing adjustments to fit changing market conditions or personal financial goals.

- 1-Year Accounts: Transfer options are available every year.

- 6-Year Accounts: Transfer options are available every six years.

Additionally, policyholders can transfer funds to the Declared Rate Account at any time during the interest term.

In my opinion, based on the latest rate sheet available at the time of writing/updating this article (May 2025), the 6-year S&P 500 with a 20% buffer offers one of the most compelling combinations of risk and return. This option provides a 100% participation rate on the S&P 500 Index, which is a decent offering in the RILA space, along with a 20% buffer to protect against market downturns. Given historical market trends, it is less likely that the S&P 500 will decline by more than 20% over a 6-year period, making this strategy a balanced and prudent choice.

That said, other S&P 500 strategies can also be considered, depending on your market outlook and risk tolerance. When selecting a strategy, it’s essential to balance risk and return. Avoid going for the least risky option (as it may significantly limit potential returns) or the most aggressive option (since it can expose you to greater losses with lower chances of reaching the cap rate).

For example, the company offers a 10.30% cap rate for a strategy with a 5% floor on the S&P 500, and a 13.25% cap rate for a 10% floor. While the 13.25% cap rate seems attractive, it requires you to take on an additional 5% risk in losses. Considering that the average annualized return of the S&P 500 from 2003 to 2023 was approximately 10%, taking on the extra 5% of floor risk for a potential 3% increase in the cap rate may not be worth it.

Additionally, given the strength and historical performance of the S&P 500 strategies, I would be inclined to avoid allocating funds to the other indices offered (like the Barclays Risk Balanced Index or the Dimensional US Small Cap Value Index). The S&P 500 is a well-diversified, large-cap index with a proven track record, while the other indices may introduce additional complexity and unpredictability.

Free Withdrawal and Surrender/Early Withdrawal Charges

Each year, you are allowed a 10% free withdrawal of your contract value, excluding any non-vested premium bonuses, without incurring charges, fees, or penalties.

Should your needs change unexpectedly, and you need to take an excess withdrawal (a withdrawal that is above the free withdrawal amount available in a given contract year), you may be entitled to access additional monies, although certain charges and penalties may apply. Any amount withdrawn in excess of the remaining free withdrawal amount is subject to a Surrender Charge. Below is the Surrender Charge schedule for the TruStage ZoneChoice Annuity:

| Contract Year | 1 | 2 | 3 | 4 | 5 | 6 | 7+ |

|---|---|---|---|---|---|---|---|

| 10-Year Plan | 8% | 8% | 8% | 7% | 6% | 5% | 0% |

Market Value Adjustments - In case you need to surrender your policy, a Market Value Adjustment (MVA) will be applied to the portion of the withdrawal or surrender that exceeds the free withdrawal amount during the withdrawal charge period. The surrender charge schedule is different for the different tenures of annuities and also changes for some states.

The surrender charge of the TruStage ZoneChoice Annuity is in line with all the other annuity issuers.

Contract/Administrative Charge

Riders and waivers

Riders and waivers

Like most annuities, the TruStage ZoneChoice Annuity includes free nursing home and confinement waiver riders designed to provide flexibility and support during critical times. These features enhance the annuity's value by allowing access to funds without penalties in specific situations:

Policyholders can access their full contract value without surrender charges or Market Value Adjustments (MVA) under the following conditions:

- Nursing Home or Hospital Confinement: If the policyholder is confined to a nursing home or hospital for 180 consecutive days after the annuity is issued.

- Terminal Illness Diagnosis: If diagnosed with a terminal illness, and the policyholder has a life expectancy of less than one year.

The TruStage ZoneChoice Annuity is designed to meet the needs of a diverse group of investors seeking both growth potential and protection from market losses. With its customizable blend of buffers, floors, participation rates, and caps, it offers a level of control that appeals to a variety of financial goals and risk tolerances. Below, we outline who is most likely to benefit from this annuity.

- Pre-Retirees and Retirees Seeking Customizable Risk and Reward: Ideal for those seeking lifetime income with protection against market losses, but with the potential for upside growth.

- Investors Seeking Market Participation With Loss Protection: Suitable for those who want to participate in market gains while using buffers or floors to limit potential losses.

- Investors With a Medium to Long-Term Investment Horizon: Best for those who can commit funds for 6 years to maximize growth potential through higher participation rates.

- Those Seeking Tax-Deferred Growth: Provides tax-deferred growth, making it a good option for those looking to reduce current tax liabilities while growing wealth.

While the ZoneChoice Annuity offers plenty of customization and protection features, it may not suit everyone. Here’s who might want to reconsider:

- Individuals Seeking Maximum Growth: The use of caps, buffers, and floors may limit upside growth, which could be less appealing to those looking for unlimited market participation.

- People With Short-Term Liquidity Needs: Withdrawals beyond the 10% free withdrawal limit are subject to surrender charges and interest adjustments, which may not work for those needing frequent access to funds.

- Young Investors: Younger individuals with a longer time horizon may prefer more aggressive growth-focused investments, such as equities or ETFs, rather than a structured annuity.

Carrier

Company details

You must always keep in mind that, unlike CDs, annuities are not guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other federal insurance agency. An annuity's "guarantee" is only as strong as the insurance company that issues the annuity, so it is always important to assess the issuing company before buying an annuity.

CMFG Life Insurance Company

CMFG Life Insurance Company, operating under the brand name TruStage Financial Group (formerly known as CUNA Mutual Group), is a mutual insurance company that provides financial services to cooperatives, credit unions, their members, and other customers worldwide. Founded in 1935 as the CUNA Mutual Insurance Society, the company has grown to serve over 30 million consumers through its lending, retirement, and wealth management products. TruStage Financial Group offers a broad range of insurance and investment products, including commercial and personal insurance, lending services, wealth management, and retirement solutions. Its insurance arm, TruStage, provides various products such as whole and term life insurance, accidental death and dismemberment insurance, auto insurance, property insurance, and annuities. Headquartered in Madison, Wisconsin, the company employs nearly 3,700 people across multiple locations in the United States and internationally.

It is rated as follows by the rating agencies:

| Rating Agency | Rating |

|---|---|

| AM Best | A |

| Moody's | A2 |

| S&P | A+ |

Going by the ratings, it is considered to be strong and stable financially. As of December 2024, some of the financial highlights for CMFG Life Insurance Company include its:

- $47.7 billion in Assets

- $3.05 billion in policyholder surplus

- $5.6 billion in total sales

- $214 million in net income

Going by the operating history, financial numbers, and ratings, we can safely gauge that you can trust your savings with the CMFG Life Insurance Company.

Conclusion

Conclusion

People are living longer, which means retirement savings may need to last longer too. A good annuity fit should protect principal, offer a reasonable path for growth, and make income options clear without hiding the trade-offs.

The TruStage ZoneChoice Annuity is a Registered Index-Linked Annuity (RILA) that offers a tailored blend of growth potential, downside protection, and customization. With options for 1-year and 6-year term accounts, policyholders can choose between flexibility and higher growth potential. Its unique combination of buffers, floors, and participation rates allows investors to balance risk and reward based on their financial goals and market outlook. While the product provides strong growth opportunities, features like caps on returns and the lack of inflation-adjusted payments may be less appealing to those seeking unlimited growth or inflation protection.

Overall, the TruStage ZoneChoice Annuity is a decent option for individuals looking for a flexible, cost-effective RILA with no contract fees, health hardship access, and a customizable approach to market risk. As always, it's important to consult a financial advisor to ensure this product aligns with your long-term investment and retirement strategy.