How it works

Symetra Trek Frontier Registered Index-linked Annuity (RILA): product description and policy

The Symetra Trek Frontier Registered Index-linked Annuity (RILA) is designed to provide policyholders with flexibility, growth potential, and a level of downside protection. It is best suited for individuals seeking higher growth potential than a fixed indexed annuity, with customizable downside protection to limit losses. It appeals to pre-retirees and retirees who want market exposure while maintaining control over their risk level. Let’s have a look at the high-level fine print of the Symetra Trek Frontier Registered Index-linked Annuity (RILA), and then we will discuss each point in detail.

| Product Name | Symetra Trek Frontier Registered Index-linked Annuity (RILA) |

|---|---|

| Issuing Company | Symetra Life Insurance Company |

| AM Best Rating | A (3rd of 13 ratings) |

| Withdrawal Charge Period(s) | 6 years |

| Maximum Issue Age | 80 Years |

| Minimum Initial Purchase Amount | $25,000 |

| Crediting Period and Strategies | - 6-year point-to-point with cap rate - 1-year point-to-point with cap rate - 1-year fixed with interest rate guaranteed |

| Plan Types | - IRA - Roth IRA - Nonqualified Account - SEP IRA - SIMPLE IRA - 401(a) |

| Indexes | - S&P 500 Index - Russell 2000 Index - Nasdaq-100 Index |

| Free Withdrawals | 15% of the annuity’s Accumulated Value per year |

| Death Benefit | Return of Purchase Payment or Contract Value, whichever is higher, without any surrender charges |

| Free Benefits | - Nursing Home and Terminal Illness Waiver |

| Optional Benefits | Return lock option |

| Surrender Value | Account Value less any withdrawal charges/MVA |

How Does the Symetra Trek Frontier Registered Index-linked Annuity (RILA) Work?

The Symetra Trek Frontier is a Registered Index-Linked Annuity (RILA) that provides a combination of market-linked growth, downside protection, and customizable features. It allows policyholders to balance risk and reward by selecting from multiple allocation options, including indexed and fixed-rate accounts. Here’s a detailed breakdown of how it works:

Initial Setup and Funding

- Minimum Payment: $25,000

- Maximum Payment (Without Prior Approval): $1,000,000

- Issue Age: 0 to 80 years old

- Plan Types: Traditional IRA, Roth IRA, SEP IRA, Beneficiary IRA, Non-Qualified, Non-Qualified Beneficiary (Stretch)

After making an initial payment, policyholders have the flexibility to choose how their funds will be allocated across various indexed accounts or the fixed rate account. These allocation choices play a major role in how the annuity performs over time. Apart from the regular crediting period, there are various events that may trigger earnings credit: On free withdrawals, for a long-term care event or terminal illness or injury event, or when a death benefit is payable. All these interest credits are credited to a bucket called “Account Value.” This bucket is your annuity account balance, and all your withdrawals take place from it.

The Symetra Trek Frontier Registered Index-linked Annuity (RILA) offers the annuitant to choose from one or more of the three indexes (S&P 500 Index, Russell 2000 Index, and Nasdaq-100) to determine their earnings crediting formula:

- The Standard & Poor's 500 (S&P 500) is a stock market index that tracks the performance of 500 large-cap U.S. companies across various industries. It serves as a key indicator of the overall health of the U.S. equity market and is widely used as a benchmark for investment performance.

- The Russell 2000 Index, on the other hand, focuses on approximately 2,000 small-cap U.S. companies, offering exposure to emerging businesses across diverse sectors. Unlike the large-cap focus of the S&P 500, the Russell 2000 captures the growth potential of smaller, more dynamic companies, making it suitable for investors looking for higher growth opportunities, albeit with increased volatility. This index serves as a benchmark for small-cap equity performance and can help diversify an annuity portfolio with exposure to companies that may have significant expansion potential.

- The Nasdaq-100 Index includes 100 of the largest non-financial companies listed on the Nasdaq Stock Market, with a strong focus on technology-driven firms. This index is heavily weighted toward innovative industries such as software, e-commerce, and biotechnology, providing annuitants with the opportunity to participate in the growth of some of the world’s most advanced and high-performing companies. While the Nasdaq-100 offers the potential for higher returns, it may also come with greater volatility due to the concentration in the tech sector.

Choosing the right index for an annuity strategy depends on an individual's financial goals and risk tolerance. The S&P 500 provides steady and consistent returns, the Russell 2000 offers exposure to smaller, high-growth companies, and the Nasdaq-100 delivers opportunities for significant appreciation driven by technological innovation. By diversifying across these indexes, policyholders can achieve a well-balanced strategy that aligns with their long-term retirement objectives.

Account Options

The allocation can be spread across multiple risk-controlled accounts and one Fixed Rate Account. These include a mix of 1-year and 6-year term accounts. The 6-year accounts offer the potential for higher returns through cap rates, while the 1-year accounts provide more flexibility by allowing annual adjustments and lock-in gains.

Rates and costs

Rates, bonus, surrender charges, and costs

The Earnings Crediting Formula

The earnings crediting formula is the most important part of this annuity discussion. It is important to know that we don’t simply get the index return credited to our annuity. There are a few caps and other rates that the company has in place that affect your earnings. These rates tend to change over time, and the updated rates can always be checked on the company’s website.

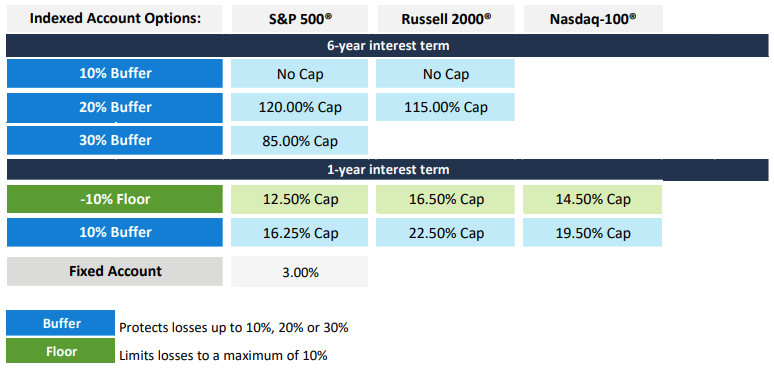

Let’s have a look at the Symetra Trek Frontier Registered Index-linked Annuity (RILA) rate sheet (as of the date of updating this article) to understand how the earnings are determined.

From the above rate chart, you will notice that there are three indexes and multiple interest-crediting options tied to those indexes. Let’s have a look at different terms that are used by the company in the Symetra Trek Frontier Registered Index-linked Annuity (RILA) rate chart:

Cap Rate

This refers to the rate at which your interest-earning capacity is capped. For example, if an index returns 12% but the contract’s cap rate is 8%, the annuitant will be eligible for an interest credit of 8% only. It doesn’t matter how much the index goes above the cap rate; the maximum interest that can be earned is the cap rate.

Cap Rate simulator

Shows how a cap limits the credited return when the index year is higher than the selected cap.

8%

Formula

min(10%, 8%) = 8%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

Fixed Account Rate

If you opt for a fixed account rate, you simply earn the fixed rates for a particular period specified by the company before your policy begins. These rates are usually low/at par as compared to other fixed avenues, such as CDs and MYGAs, so you should avoid fixed rates in a general scenario. The 1-year fixed rate on this policy at the time of writing this article was 3.00%.

Risk and Reward Control Customization

The Symetra Trek Frontier Registered Index-linked Annuity (RILA) offers various crediting strategies that allow annuity holders to customize their exposure to market risk and reward. Below is an explanation of the terms in the rate chart, along with an example to demonstrate how they function:

- Buffer: The buffer is the percentage of market loss that Symetra absorbs during the crediting period. For example, a 10% buffer means that if the market declines by up to 10%, the annuity holder does not incur any losses. However, if the market loss exceeds the buffer, the policyholder’s account value will be reduced by the excess loss.Example:Market decline: 12%Buffer: 10%Loss incurred by policyholder: 2% (12% - 10%)

- Floors: A floor sets the maximum amount of loss the policyholder is willing to absorb. Losses below this limit are absorbed by the insurer.Example: With a -10% floor, if the market drops 30%, the policyholder only loses 10%, and the remaining 20% loss is absorbed by the insurer.

- Return Lock FeatureThis feature allows policyholders to lock in gains by setting an Interim Value at any point during the crediting period, free of charge.Policyholders can choose between two options:Predefined Target: Set a growth target at the beginning of the crediting period for automatic lock-in when the target is reached.Manual Lock-In: Manually lock in gains at any time during the journey if market conditions are favorable.Once the Return Lock is activated, additional index gains or losses will not affect the account until the next allocation anniversary. After the lock-in period, policyholders can reallocate to any available index strategy without having to wait for the end of the current crediting period.

The Return Lock is useful when you want to secure gains during favorable market conditions and protect your earnings from potential future market downturns, especially if you believe that the index has peaked for this crediting period, allowing you to lock in returns without waiting for the full term to end.

Among the available indexing strategies, the following options stand out to me:

- 6-Year S&P 500 Index with 10% Buffer and Unlimited Cap Rate: This strategy is appealing due to its strong index, decent buffer, and higher cap rate, which allows for enhanced upside potential while providing partial downside protection.

- 6-Year Russell 2000 Index with 10% Buffer and Unlimited Cap Rate: This strategy provides access to very high cap rates on a 6-year cycle with a decent 10% buffer.

- 1-Year Russell 2000 with 10% Floor and 16.50% Cap Rate: This strategy is appealing due to its strong index, decent floor, and good cap rate, which allows for returns even during the period of negative index returns up to 10%.

- 1-Year Nasdaq-100 Index with 10% Buffer and 19.50% Cap Rate: This strategy is appealing due to its strong index, decent buffer, and good cap rate, which allows for less risky upside potential while providing decent downside protection.

You have the flexibility to allocate your premium across multiple crediting strategies, allowing you to diversify your growth potential based on different market indices and risk levels. This enables a balanced approach by combining strategies with varying buffers, participation rates, and cap structures.

Free Withdrawal and Surrender/Early Withdrawal Charges

Each year, you are allowed a 15% free withdrawal of your contract value, excluding any non-vested premium bonuses, without incurring charges, fees, or penalties.

Should your needs change unexpectedly, and you need to take an excess withdrawal (a withdrawal that is above the free withdrawal amount available in a given contract year), you may be entitled to access additional monies, although certain charges and penalties may apply. Any amount withdrawn in excess of the remaining free withdrawal amount is subject to a Surrender Charge. Below is the Surrender Charge schedule for the Symetra Trek Frontier Registered Index-linked Annuity (RILA):

| Contract Year | 1 | 2 | 3 | 4 | 5 | 6 | 7+ |

|---|---|---|---|---|---|---|---|

| 10-Year Plan | 8% | 8% | 7% | 6% | 5% | 4% | 0% |

Market Value Adjustments - In case you need to surrender your policy, a Market Value Adjustment (MVA) will be applied to the portion of the withdrawal or surrender that exceeds the free withdrawal amount during the withdrawal charge period. The surrender charge schedule is different for the different tenures of annuities and also changes for some states.

The surrender charge of the Symetra Trek Frontier Registered Index-linked Annuity (RILA) is in line with all the other annuity issuers.

Contract/Administrative Charge

Free Riders and Benefits

Like most annuities, the Symetra Trek Frontier Registered Index-linked Annuity (RILA) includes several free benefits designed to provide financial flexibility and support during critical times. These features allow policyholders to access their funds without penalties under specific conditions, enhancing the annuity’s overall value. Policyholders can access their full contract value without incurring surrender charges or Market Value Adjustments (MVA) under the following conditions:

- Nursing Home or Hospital Confinement: Applies if the policyholder is confined to a nursing home or hospital for 30 consecutive days after the annuity is issued.

- Terminal Illness Diagnosis: Applies if the policyholder is diagnosed with a terminal illness and has a life expectancy of less than one year.

Carrier

Company details

You must always keep in mind that, unlike CDs, annuities are not guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other federal insurance agency. An annuity's "guarantee" is only as strong as the insurance company that issues the annuity, so it is always important to assess the issuing company before buying an annuity.

Symetra Life Insurance Company

Symetra Life Insurance Company, established in 1957, is a U.S.-based provider of retirement plans, employee benefits, annuities, and life insurance. Headquartered in Bellevue, Washington, Symetra operates through a network of independent distributors nationwide. In 2016, Symetra was acquired by Sumitomo Life Insurance Company, one of Japan's leading life insurers, for $3.8 billion. This acquisition has strengthened Symetra's financial foundation, enabling strategic growth and product development.

Symetra offers a diverse range of products tailored to individuals and businesses:

- Life Insurance: Term life, indexed universal life, and variable universal life policies designed to provide financial protection and flexibility.

- Annuities: Fixed, fixed indexed, and immediate annuities aimed at delivering stable income streams for retirement planning.

- Employee Benefits: Group life, disability, and medical stop-loss insurance solutions catering to employers seeking comprehensive benefits packages.

It is rated as follows by the rating agencies:

| Rating Agency | Rating |

|---|---|

| AM Best | A |

| Moody's | A1 |

| S&P Global | A |

Symetra Life Insurance Company’s financial strength is reflected in the following figures as of FY2024:

- Total Assets: $68.4 billion

- Investment Portfolio: $55.4 billion

- Investment Grade Portfolio: 95.6%

- Stockholders’ Equity: $2.6 billion

- Employees: 2600+

Going by the operating history, financial numbers, and ratings, we can safely gauge that you can trust your savings with the Symetra Life Insurance Company.

Conclusion

Conclusion

With the advancement in healthcare and technology, the average person today is living longer than ever. So, it’s very important to have a stream of income that can grow safely and steadily and have the ability to provide a guaranteed income during the retirement years. This not only helps you mitigate the risk of outliving your income but also ensures that you continue to live a decent life even in your retirement.

The Symetra Trek Frontier Registered Index-Linked Annuity (RILA) offers a balanced approach to retirement planning by combining market-linked growth potential with built-in downside protection features. The Trek Frontier RILA offers flexibility with multiple indexing options, including the S&P 500, Nasdaq-100, and Russell 2000, catering to different risk appetites and financial goals. Whether investors prioritize stable returns with strategies like the high buffer rates or aim for higher accumulation through enhanced participation, the Trek Frontier RILA provides a versatile solution. However, it's important for potential buyers to carefully evaluate their risk tolerance, growth expectations, and fee implications to determine if this product aligns with their long-term retirement strategy.