Introduction

For beneficiaries, it’s important to understand all the costs associated with Medicare. The numerous factors to consider include: the timing of when to enroll for Medicare, the four different parts of Medicare, what is covered in each, premiums, etc. This series of articles aims to introduce and explain a lesser-known factor when planning for health care with Medicare, the income-related monthly adjusted amount or IRMAA.

Per the Social Security Administration, “The income-related monthly adjustment amount (IRMAA) sliding scale is a set of statutory percentage-based tables used to adjust Medicare Part B and Part D prescription drug coverage premiums. The higher the beneficiary’s range of modified adjusted gross income (MAGI), the higher the IRMAA.” (Social Security Administration, 2024)

IRMAA was enacted into law by Congress in 2003. This was to help ensure the solvency of the program by making higher earning beneficiaries bear more of the burden for it. The merits of this can be debated but the fact of the matter is that IRMAA is here for the long haul.

Although the average income for Americans 65 and older is $75k (Streeter, 2024) and the IRMAA does not kick in until MAGI reaches $103k (or $206k for filing jointly), there are still 23% of households 65 and older who qualify for IRMAA based on their income (US Census Bureau, 2024). Also to be considered is the fact that the SSA will use the MAGI from two years prior (three if no data is available) to determine IRMAA qualification. For example, for 2024 the SSA will use the tax filers 2022 returns to determine income (or 2021 if 2022 is not available). For 2024 beneficiaries, their current income may not exceed the $103k threshold, however, since they were probably working the two years prior their MAGI used in the IRMAA calculations will be higher for the first two years of their retirement. This is important to consider when planning for retirement and determining when to enroll for Medicare.

Many beneficiaries will choose to perform an IRA conversion ladder during their retirement (Folger, 2024). Especially if they are retiring early or have most of their retirement savings wrapped up in traditional 401k’s or IRAs. When converting traditional 401k’s and IRAs to Roth IRAs, the money that is converted will count as earned income, thus raising the MAGI for the beneficiary in that year. If the beneficiary is not careful, they may end up reaching the $103k or $206k threshold, thus triggering IRMAA.

Another scenario is for beneficiaries 73 or older. At this age, required minimum distributions kick in. This is a big reason why many beneficiaries are subject to IRMAA.

How IRMAA is Calculated and How to Determine if You Owe

As discussed, IRMAA thresholds are determined from the tax returns two years prior to the current year. From the tax filings, Modified Adjusted Gross Income (MAGI) is used to determine IRMAA costs.

Your MAGI is NOT a line item on your tax return but can be calculated from the items on the return. MAGI is the total of the following for each member of your household who’s required to file a tax return (Department of Health and Human Services, 2024):

- Adjusted Gross Income (AGI) on federal tax return (IRS Form 1040, Line 11)

- Excluded foreign income

- Nontaxable Social Security benefits (including tier 1 railroad retirement benefits)

- Tax-exempt interest

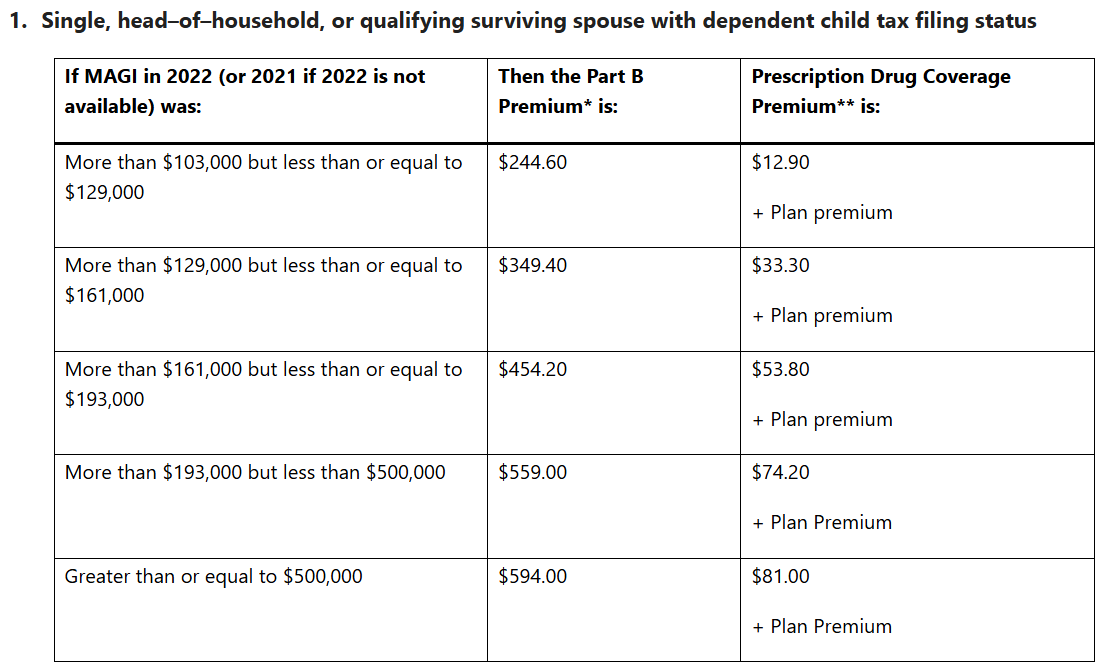

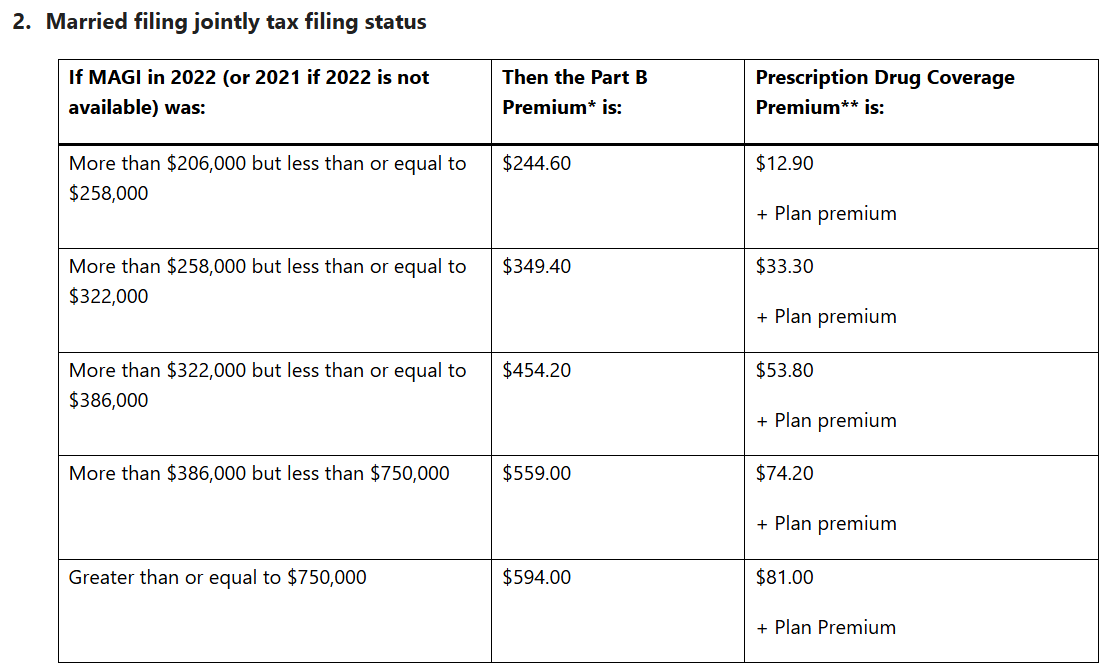

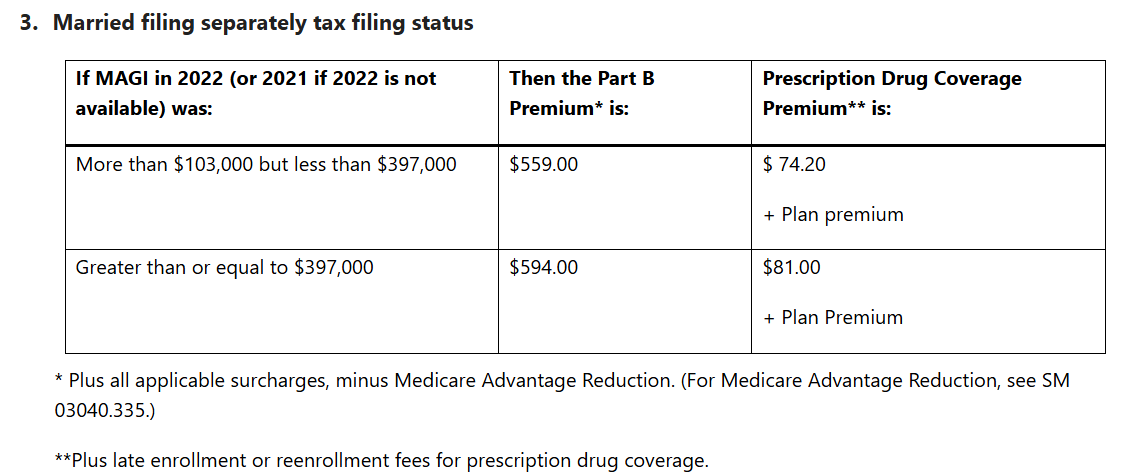

Healthcare.gov has a table of income types that is included in MAGI. Once the beneficiary’s MAGI, from the correct filing year is calculated, the beneficiary can use the tables provided by the SSA to determine their IRMAA premium. There are three tables that are used. The tables are categorized by tax filing status: Single, head–of–household, or qualifying surviving spouse with dependent child, Married filing jointly and Married filing separately. Tables for 2024 are shown below. (Social Security Administration, 2024)

If IRMAA applies to a beneficiary, the Social Security Administration will send out a notice. These notices can come at any time. These notices are stored in the Online Retrieval System. The SSA uses data from IRS to determine IRMAA applicability. There are four different notices that can come from the SSA (Social Security Administration, 2024):

| Notice | Description | Appeals Rights Disclosure? |

|---|---|---|

| Title 2 Redesign (T2R) | A Title II Redesign (T2R) notice, which is not an IRMAA specific notice, is sent with the new IRMAA information and appeal rights. | Y |

| Targeted Cost-of-Living Adjustment Notices | If MAGI is above the threshold for the upcoming premium year the beneficiary will receive a specific targeted cost-of-living adjustment (COLA) notice which explains IRMAA in detail. The targeted IRMAA COLA notice is an initial determination with appeal rights.\ The notice explains: - What information was used to compute IRMAA - What the beneficiary can do if the tax information IRS provides is wrong - What the beneficiary can do if SSA used information from a tax year that is three years prior to the premium year (PY-3) and the beneficiary has a copy of their filed tax return for the tax year that is two years prior to the premium year (PY-2) - What the beneficiary can do if the tax filing status of “Married, Filing Separately” for the tax year was used and lived apart from the spouse for the entire year - What the beneficiary can do if there was a life changing event (LCE) with a reduction in income, and - That variable SMI (VSMI) will not apply to Medicare Part B beneficiaries who must pay IRMAA. | Y |

| Pre-Determination Notice | New Medicare filers and attainers will be charged the standard Part B premium or the prescription drug plan premium without an IRMAA until the SSA receives MAGI data from IRS.\ If IRS returns data indicating that a new filer’s or attainer’s MAGI is above the appropriate threshold, SSA will send a pre-determination notice.\ This notice will explain: That IRMAA will apply, - What information was used to compute IRMAA - What the beneficiary can do if the tax information provided by IRS is wrong - What the beneficiary can do if SSA used PY-3 information and the beneficiary has a copy of their filed PY-2 tax return, - What the beneficiary can do if the tax filing status of “Married, Filing Separately” for the tax year was used and lived apart from their spouse for the entire year, and - What the beneficiary can do if there was an LCE with a reduction in income. | N |

| Initial Determination Notice | When SSA makes an initial determination regarding IRMAA, SSA sends a decision notice 20 days or more after issuing the pre-determination notice to new filers and attainers. These notices contain appeal rights and inform the beneficiary to contact SSA if one of the following situations apply: - The beneficiary experienced an LCE that caused a significant reduction in MAGI (i.e. caused MAGI to go down at least one range in the tables). - SSA used PY-3 data and the beneficiary can supply a copy of the PY-2 Federal income tax return, - The beneficiary filed, and IRS accepted an amended income tax return for the year we are using to set the IRMAA, - There was an error in the information provided to SSA by IRS and the beneficiary can provide proof from IRS acknowledging the error and the correction, or - The beneficiary had a filing status of “Married, Filing Separately” and reports living apart from their spouse at all times during that tax year. | Y |

Another article in this series will deal with what to do if an appeal is necessary.

Medicare Parts Affected

Medicare is Federally provided health care for Americans 65 and older. Medicare is broken into four parts (Department of Health and Human Services, 2024):

| Parts | Description |

|---|---|

| A | Helps cover inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. |

| B | Helps cover: Services from doctors and other health care providers Outpatient care Home health care Durable medical equipment (like wheelchairs, walkers, hospital beds, and other equipment) Many preventive services (like screenings, shots or vaccines, and yearly “Wellness” visits) |

| C (Medicare Advantage) | Medicare Advantage is a Medicare-approved plan from a private company that offers an alternative to Original Medicare for your health and drug coverage. These “bundled” plans include Part A, Part B, and usually Part D. |

| D | Helps cover the cost of prescription drugs |

IRMAA premiums only apply to Parts B and D. Beneficiaries on Medicare Advantage (Part C) are also included if their MAGI meet the SSA thresholds. This is because Medicare Advantage members still pay the Part B premium along with any applicable IRMAA charges.

Conclusion

Retirement planning can at times be as clear as mud! Especially when dealing with the federal government. However, this series of articles aims to clear the waters on at least one topic germane to a large segment of Medicare beneficiaries. The next article will discuss ways to reduce or avoid IRMAA surcharges. These articles will try to cover the basics, but for further advice on your specific financial journey it is recommended to seek out a professional advisor.

References

Folger, J. (2024, July 26). How the Roth Conversion Ladder Works. Retrieved from Investopedia

Related on AnnuityRatesHQ