How it works

Delaware Life Target Growth Fixed Indexed Annuity: product description and policy

The Delaware Life Target Growth is a Fixed Indexed Annuity (FIA) plan that offers the annuitant (annuity investor) an opportunity to earn a part of market index-linked return without having to incur the risk of market downside. This is a suitable plan for individuals seeking a fixed-indexed annuity that provides tax-deferred growth and downside protection, with a primary focus on income growth.

Let’s have a look at the high-level fine print of the Delaware Life Target Growth Fixed Indexed Annuity, and then we will discuss each point in detail.

| Product Name | Target Growth 10 |

|---|---|

| Issuing Company | [Delaware Life Insurance Company](https://annuityrateshq.com/reviews/delaware-annuity-reviews) |

| AM Best Rating | A- (4th of 13 ratings) |

| Withdrawal Charge Period(s) | 10 years |

| Maximum Issue Age | 80 Years |

| Minimum Initial Purchase Amount | $25,000 |

| Crediting Period and Strategies | - 1-year point-to-point with participation rate - 1-year point-to-point with caps - 1-year performance trigger - 1-year fixed with interest rate guaranteed |

| Plan Types | - IRA - Roth IRA - Nonqualified Account - SEP IRA - SIMPLE IRA - 401(a) |

| Indexes | - S&P 500 Index - S&P 500 Dynamic Intraday TCA Index - First Trust Capital Strength Barclays 10% Index - Goldman Sachs Canopy Index - Franklin SG Select Index - Nasdaq 100 Intraday Elite 15% Index |

| Free Withdrawals | 10% of the annuity’s Accumulated Value per year |

| Death Benefit | Upon the annuitant’s death, the beneficiary will get greater of (i) Account Value or (ii) Surrender Value |

| Free Benefits | - Guaranteed Minimum Account Value (GMAV) - Nursing Home and Terminal Illness Waivers |

| Surrender Value | Account Value less any withdrawal charges/MVA |

| RMD Friendly | Yes |

How does the Delaware Life Target Growth Fixed Indexed Annuity policy work?

An annuitant (maximum age at the time of policy issue: 80) can purchase the Delaware Life Target Growth Fixed Indexed Annuity with a minimum initial purchase amount of $25,000, and in return, they will earn market index returns (calculated through a formula that we will discuss shortly), credited as per the chosen crediting period. Apart from the regular crediting period, there are various events that may trigger earnings credit: On free withdrawals, for a long-term care event or terminal illness or injury event, or when a death benefit is payable.

The Delaware Life Growth Fixed Indexed Annuity offers the annuitant to choose from one or more of the six indexes (S&P 500 Index, S&P 500 Dynamic Intraday TCA Index, First Trust Capital Strength Barclays 10% Index, Goldman Sachs Canopy Index, Franklin SG Select Index, and Nasdaq-100 Intraday Elite 15% Index) to determine their earnings crediting formula. The S&P 500 index has 3 crediting strategies, and the other five indexes have one strategy each. The plan also offers a fixed-rate guaranteed interest strategy to choose from, making a total of 9 strategy options. We will discuss each available index briefly:

1. S&P 500 Index

The S&P 500 index is one of the most popular and oldest indexes in the world. It tracks 500 large-cap publicly traded stocks listed in the United States. It is a reliable index and has often succeeded in the test of time. It is very important to note that, similar to most other annuities, the Delaware Life Target Growth Fixed Indexed Annuity offers the S&P 500 index with cap rates, participation rates, and performance-trigger rates in place, meaning that your actual interest credited will be lower compared to the actual index return. These rates change frequently; I will discuss the rates in detail shortly.2. First Trust Capital Strength Barclays 10% IndexThe First Trust Capital Strength® Barclays 10% Index aims to provide stable growth with a diversified portfolio that provides exposure to U.S. equities and Treasurys and targets a 10% volatility. The index creates a diversified portfolio by combining U.S. stocks selected based on capital strength methodology with a portfolio of four Barclays U.S. Treasury futures indexes. The Index tries to limit long-term realized volatility to 10% or less, dynamically adjusting the allocation between the underlying traded instruments and cash, which can reduce the overall rate of return compared to indexes without a volatility control mechanism.3. Goldman Sachs Canopy IndexThe Goldman Sachs Canopy Index is a USD excess return index designed to combine a traditional asset allocation strategy with an alternative investment approach. It aims to diversify returns by providing exposure to two distinct portfolios: (i) A long-only "Core Portfolio" consisting of traditional assets like equities, U.S. Treasury bonds, Treasury Inflation-Protected Securities (TIPS), commodities, and gold. (ii) A long-short "Satellite Portfolio" employing market-neutral strategies.The index adjusts the weights of assets in the Core Portfolio based on market growth and inflation signals, while maintaining fixed weights for the alternative assets in the Satellite Portfolio. It also incorporates a volatility control mechanism targeting 8% volatility. Launched in March, 2024, the index aims to provide exposure to market performance while offering potential diversification benefits through its alternative investment component.4. Franklin SG Select IndexThe Franklin SG Select Index is designed to deliver stable returns by dynamically adjusting its investment strategy across changing market conditions. It offers exposure to top-performing large and mid-cap U.S. stocks selected from Franklin Templeton's mutual fund universe. The index employs a multi-factor investing approach, focusing on value, quality, and momentum to identify stocks with strong growth potential. To manage risk, the index incorporates a volatility control mechanism targeting 5% annual volatility and adjusts its exposure by shorting an ETF tracking the S&P 500 Index. Additionally, it diversifies with 10-year U.S. Treasuries, adjusting bond allocations based on market conditions to further stabilize returns. This approach aims to protect against market downturns but also limits the index upside.5. Nasdaq-100 Intraday Elite 15% IndexThe Nasdaq-100 Intraday Elite 15% Index is a rules-based strategy that starts with the Nasdaq-100 universe and applies an intraday rebalancing process designed to capture short-term market momentum while managing daily volatility. The index targets a 15% volatility level, meaning it adjusts its exposure throughout the day—scaling up during calmer periods and reducing exposure when markets are more turbulent. Because of this built-in volatility control, the index tends to deliver smoother but more constrained returns compared to the traditional Nasdaq-100.6. S&P 500 Dynamic Intraday TCA IndexThe S&P 500 Dynamic Intraday TCA Index is a financial index designed to provide exposure to the S&P 500 through the use of E-mini S&P 500 futures. This index employs a dynamic approach, utilizing 13 observation windows throughout the trading day to adapt to changing market conditions. By doing so, it aims to offer a more stable volatility experience for investors. The index combines a trend-following mechanism with the capability to rebalance multiple times during the day, allowing it to respond swiftly to market movements and optimize performance.

It is very important to note that, like other Fixed Indexed Annuities, the Delaware Life Target Growth Fixed Indexed Annuity comes with cap rates, participation rates, performance triggers, etc., for these indexes, meaning that you will be credited only a part of the index return to your annuity. These rates change frequently; I will discuss them more shortly.

Note: In addition to allocating the funds in the following indexes, the annuitant also has the option to allocate funds at a fixed interest. These Fixed Rates change from time to time. The Fixed Value Rate for the 10-year withdrawal charge period at the time of writing this article was 4.60% (for the $100,000 and over band).

At the time of this review (Nov 2025), this was the published figure. For current rates, see Current Rates ↑.

Rates and costs

Rates, bonus, surrender charges, and costs

The Earnings Crediting Formula

The earnings crediting formula is the most important part of this annuity discussion. It is important to know that we don’t simply get the index return credited to our annuity. The company has several rate-limiting mechanisms, including cap rates, participation rates, and performance triggers, that affect our earnings. These rates are subject to change over time, and you can check the updated rates with your financial advisor or on the company’s website.

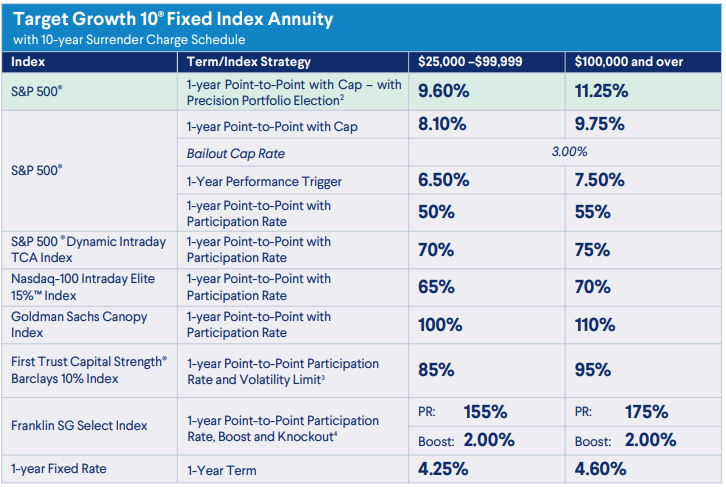

Let’s have a look at the Delaware Life Target Growth 10 Fixed Index Annuity rate sheet (as of November 2025) to understand how the earnings are determined.

From the above rate chart, you will notice that there are 9 interest crediting options (1 fixed and 8 indexed). Let’s have a look at different terms that the company uses in the Target Growth 10 FIA chart rate:

Cap Rate

This refers to the rate at which your interest-earning capacity is capped. For example, if an index returns 12% but the contract’s cap rate is 6%, the annuitant will be eligible for an interest credit of 6% only. It doesn’t matter how much the index goes above the cap rate; the maximum interest that can be earned is the cap rate.

Cap Rate simulator

Shows how a cap limits the credited return when the index year is higher than the selected cap.

8%

Formula

min(10%, 8%) = 8%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

Participation Rate

The participation rate describes the annuitant’s participation percentage in the return of an index. For example, suppose the participation rate is 150%, and the index returned 4% over the agreed time. In that case, the annuitant will be eligible for 150% of the return, i.e., 6%.

Participation Rate simulator

Shows how the contract credits a percentage of a positive index return.

5%

Formula

10% x 50% = 5%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

Performance Trigger Rate

Index Option with Declared Rate: A flat or positive index return triggers the declared interest rate to be credited to the contract value. If the index return is negative, no interest is credited, but there will be no loss, and the contract value will remain the same. The declared interest rate is set at contract issue and applies for the entire withdrawal charge period. In this case, the performance-triggered rate for the S&P 500 Index is 7.5%. It means that if the S&P Index doesn’t go negative for a given 1-year period (even if the growth is 0% and not negative), the interest credited to the annuity will be 7.5% irrespective of the S&P 500's actual return.

Performance Trigger Rate simulator

Shows how a flat or positive index year can credit the declared trigger rate.

6%

Trigger activates

Formula

10% is flat or positive, so the trigger credits 6%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

Participation Rate

, Boost, and Knockout: This index strategy adds a Boost Rate to the return of an index at the end of the term if a Knockout has not occurred. If a Knockout has not occurred, the company will compare the index value at the end of the term to its value at the beginning of the term and add a Boost Rate to the percentage change in the index. A Participation Rate is then applied to the boosted index return to determine the amount of interest credited. A Knockout is an event that cancels an index interest credit and occurs if the index value drops below the Knockout Barrier at any point during the term. If a Knockout occurs, you will not receive an interest credit and may not transfer your index value to another index strategy until the end of the term. For example, If the index value at the beginning of the term is 2000 and the Knockout Rate is 98%, then the Knockout Barrier value would be 1960.

Participation Rate simulator

Shows how the contract credits a percentage of a positive index return.

5%

Formula

10% x 50% = 5%

This is a one-year teaching example only. Actual contract credits depend on the index, strategy term, allocation, renewal rates, state rules, and carrier contract language.

Fixed Account Rate

If you opt for a fixed account rate, you simply earn the fixed rates for a particular period specified by the company before your policy begins. These rates are usually low/at par as compared to other fixed avenues, such as CDs and MYGAs, so you should avoid fixed rates in a general scenario. The 1-year fixed rate on this policy at the time of writing this article was 4.60%.

Bailout Provision

For the S&P 500 1-year point-to-point strategy with cap, if the company lowers any rate below the Bailout Cap rate, you’ll have full access to withdraw your annuity’s accumulated value - free of any charges or Market Value Adjustments.

Among these indexes, I prefer the S&P 500 Index with a cap option or performance trigger option. I avoid any S&P 500 strategy with a participation rate because the company offers a very low participation rate for the S&P 500 Index. The Franklin SG Select Index is also a good indexing option if you are willing to take on some risk—if the knockout barrier isn’t hit, you get a very good participation rate plus an additional boost.

You can also consider the fixed account option, as the company is currently offering one of the highest fixed rates among other annuity providers.

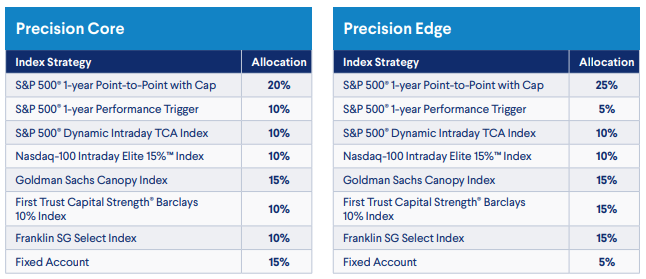

Precision Portfolios

The annuitant can also choose from two model Precision Portfolios, which are designed to offer diversification benefits without the need to select indexing strategies manually. Each portfolio is constructed with set percentage allocations to individual index strategies from providers such as S&P, Nasdaq, Goldman Sachs, First Trust, and Franklin Templeton, along with an allocation to the fixed account.

If I were to choose, I would focus solely on the S&P and Nasdaq-100 strategies, and I would opt to pass on the Precision Portfolios. However, if you plan to go for the Precision Portfolios, I would prefer Option #1 (Precision Core) because it offers broad-based indexes with a solid performance history, transparency, and strong expected returns.

Accessing your Money

Each year, you are entitled to a 10% free withdrawal of your contract value without incurring any charges, fees, or penalties.

Should your needs change unexpectedly, and you need to take an excess withdrawal (a withdrawal that is above the free withdrawal amount available in a given contract year), you may be entitled to access additional monies, although certain charges and penalties may apply. Any amount withdrawn in excess of the remaining free withdrawal amount is subject to a Surrender Charge. Below is the Surrender Charge schedule for the Target Growth 10 Fixed Indexed Annuity.

| Completed Contract Years | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11+ |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Surrender Charge % | 10% | 10% | 10% | 10% | 10% | 9% | 8% | 7% | 6% | 5% | 0% |

Market Value Adjustments - In case you need to surrender your policy, a Market Value Adjustment (MVA) will be applied to the portion of the withdrawal or surrender that exceeds the free withdrawal amount during the withdrawal charge period. The surrender charge schedule is different for the different tenures of annuities and also changes for some states.

The surrender charge of Delaware Life Target Growth Fixed Indexed Annuity is in line with all the other annuity issuers.

Once the surrender charge period ends, you can typically access your full contract value without fees. However, any withdrawal reduces both your contract value and, if applicable, the income base tied to optional riders, which may impact future guaranteed income.

An annuitant can also convert the contract into a stream of guaranteed income, known as annuitization. They can choose from various payout options designed to meet different needs.

- Life Only – Provides income for as long as you live.

- Joint and Survivor Life – Continues payments over two lifetimes, often used by couples.

- Life with Period Certain (up to 30 years) – Pays income for life, but guarantees payments for a minimum period even if death occurs earlier.

- Period Certain (up to 30 years) – Provides guaranteed payments for a set number of years, regardless of lifespan.

- Single Life or Joint Life with Cash Refund – Ensures that if the annuitant(s) pass away before receiving payments equal to the original premium, the difference is refunded to beneficiaries.

- Single Life or Joint Life with Installment Refund – Similar to the cash refund, but any remaining balance is paid out over time in installments.

These options allow flexibility in balancing lifetime income needs with legacy goals, offering a way to customize how and when funds are accessed in retirement.

Death Benefit

Upon the annuitant’s death, the beneficiary will get the greater of (i) the Account Value or (ii) the Surrender Value

Riders and waivers

Riders and waivers

The Target Growth 10 is a plain-vanilla annuity that does not offer any optional paid riders. In my opinion, this actually appeals to many people who don’t understand or do not want to dive deep into the complex methodologies the riders often come up with. However, as with most annuities, the Target Growth 10 has free in-built nursing home and terminal illness waivers.

Nursing Home Waiver: After the first contract year, an annuitant can withdraw up to 100% of the contract’s accumulated value if he is confined to a Qualified nursing home for at least 90 consecutive days. No withdrawal charge or MVA applies if the owner qualifies for this benefit. Diagnosis must occur after the contract is issued, and written proof with supporting documentation is required from a qualified physician.

Terminal Illness Waiver: After the first contract year, an annuitant can withdraw up to 100% of the contract’s accumulated value if he is diagnosed with a terminal illness with a prognosis of 12 months or less. No withdrawal charge or MVA applies if the owner qualifies for this benefit. Diagnosis must occur after the contract is issued, and written proof with supporting documentation is required from a qualified physician.

Besides the Nursing Home Waiver and the Terminal Illness Waiver, the company also offers a Guaranteed Minimum Account Value (GMAV) provision.

Guaranteed Minimum Account Value (GMAV) - The Guaranteed Minimum Account Value (GMAV) provision ensures that the account value of your annuity will be no less than 125% of the initial premium, adjusted for any withdrawals, upon reaching the 10-year milestone.

Suppose you invest an initial premium of $100,000 in an annuity product that offers a GMAV feature. Over the course of 10 years, you make withdrawals totaling $20,000.

Initial Premium: $100,000Total Withdrawals: $20,000Net Account Value (Initial Premium - Withdrawals): $80,000

The GMAV feature guarantees that your account value will be at least 125% of the initial premium, less any withdrawals, at the 10th anniversary.

GMAV Calculation:

125% of Initial Premium = 1.25 * $100,000 = $125,000Adjusted for Withdrawals: $125,000 - $20,000 = $105,000

Therefore, at the end of the 10-year period, the GMAV ensures that your account value will not be less than $105,000, regardless of market conditions or investment performance.

Carrier

Company details

You must always keep in mind that, unlike CDs, annuities are not guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other federal insurance agency. An annuity's "guarantee" is only as strong as the insurance company that issues the annuity, so it is always important to assess the issuing company before buying an annuity.

Delaware Life Insurance Company

Delaware Life Insurance Company was founded in 2013 and is a subsidiary of Group 1001 Insurance Holdings, LLC. Group 1001 is a dynamic network of several insurance businesses. It is a relatively newer player, but is rapidly growing and making its name in the market. In 2025, Delaware Life was top-rated in Barron’s 100 Annuities list.

It is rated as follows by the rating agencies:

| Rating Agency | Rating |

|---|---|

| AM Best | A- |

| S&P | A- |

| Fitch Ratings | A- |

Although the ratings are not the best when we compare them with bigger players, they are good enough for you to consider buying an annuity.

Delaware Life Insurance Company has managed to maintain decent ratings for many years. It is considered to be strong and stable financially. As of June 2025, the company had assets of $56.2 billion, with more than 324,000 active annuity and life insurance policies.

Going by the operating history, financial numbers, and ratings, we can safely gauge that you can trust your savings with Delaware Life Insurance Company.

Pros

The plan offers the S&P Index with multiple crediting methodologies.

Decent Cap and Participation Rates on many indexes

Free GMAV Provision

No annual contract, mortality & expense, or administrative fees

Free Confinement and Terminal Illness Waiver Benefit

This no-fee rider is automatically included for owners under age 65 and includes both a Qualified Nursing Care and Terminal Illness Benefit:

Multiple Payout Options

Lumpsum or Annuitization option with Life Only, Life with Period Certain, Joint and Survivor Life, etc.

Cons

Higher Surrender Charges

This annuity imposes relatively higher surrender charges than other similar annuities.

Although the annuity offers good strategies on the S&P 500 Index, I don’t like the other three indexes that the company offers for the interest crediting strategy. The other three indexes that the company offers have a volatility control mechanism that limits the overall return of the index.

Conclusion

Conclusion

With the advancement in healthcare and technology, the average person today is living longer than ever. So, it’s very important to have a stream of income that can grow safely and steadily and have the ability to provide a guaranteed income during retirement years. This not only helps you mitigate the risk of outliving your income but also ensures that you continue to live a decent life even in your retirement.

The Delaware Life Target Growth FIA is a decent annuity that helps you grow your retirement account with much less risk. Through its higher caps and performance-trigger rates, It offers faster growth with principal protection. The product’s plain vanilla nature (with no optional paid riders) might also appeal to people who don’t like to deep-dive into the complex methodologies often associated with the riders. However, if you are someone who is looking for enhanced lifetime withdrawals, you should consider checking out our review of the Delaware Life Target Income Fixed Indexed Annuity.